Turning 65?

A Medicare Enrollment Decision Guide

A simple guide to understanding Medicare enrollment at age 65 and avoiding costly timing mistakes.

For many people, Medicare enrollment at age 65 begins during a specific window known as the Initial Enrollment Period. This 7-month window starts three months before your 65th birthday, includes your birthday month, and ends three months after. Understanding this timing can help you avoid a Medicare Part B penalty and unnecessary coverage gaps.

Turning 65 doesn’t come with a clear instruction manual.

You’re suddenly asked to make decisions that can affect your coverage, your savings, and your future... often without clear guidance.

Certain Medicare enrollment decisions can affect things like:

- Lifetime penalties

- Lost HSA eligibility

- Paying for coverage you didn’t actually need

That’s exactly why this guide exists.

It’s designed to help you understand your options before you take action so you can move forward with clarity and confidence.

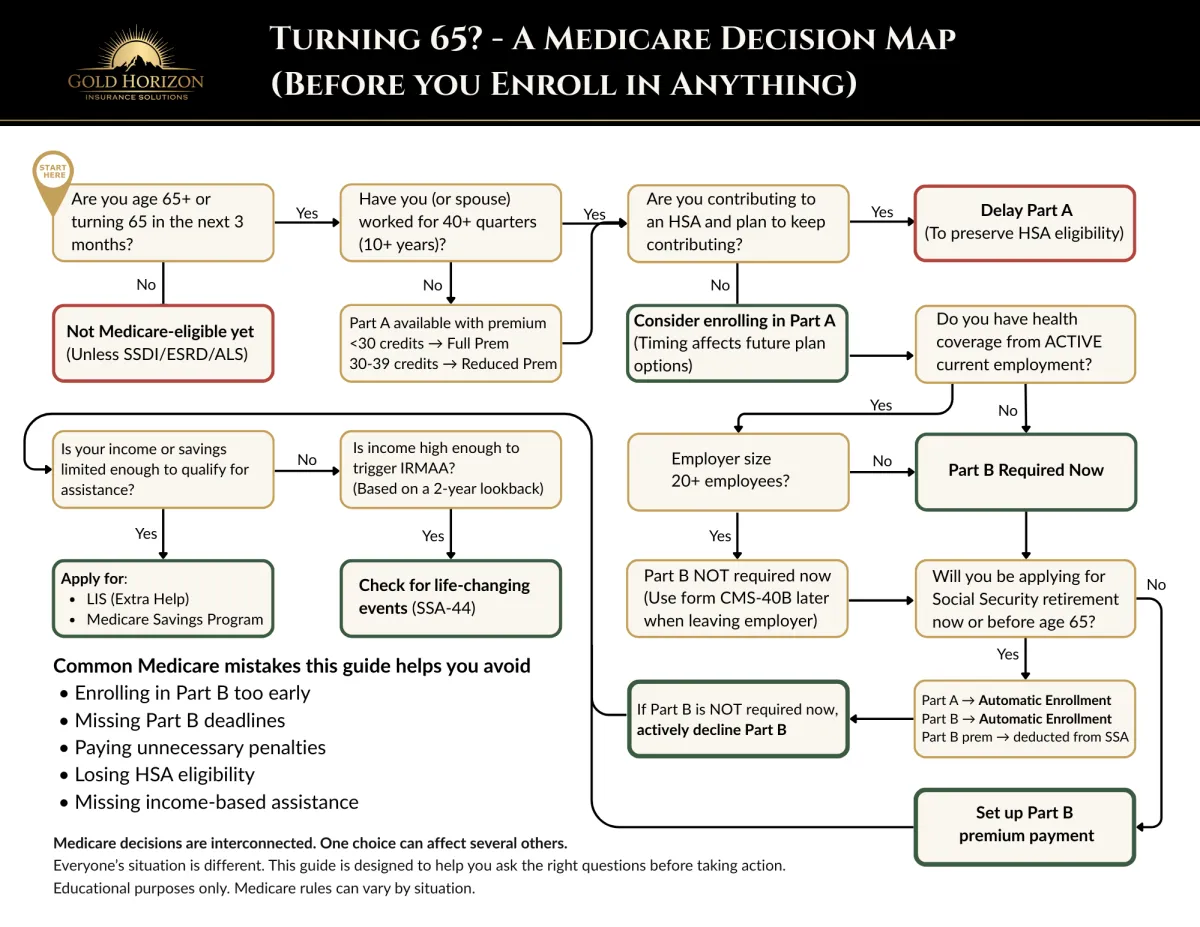

How to Use this Medicare Decision Guide:

Start at the top-left of the chart

Answer each question honestly

Follow the arrows based on your situation

When you reach a recommendation, use the resources listed below for your convenience!

Click image below to download 👇

When to enroll in Medicare depends on your employment status, income considerations, and whether you plan to delay certain parts. The goal of this guide is not to assume your situation, but to help you understand the questions that matter before decisions are made

Take Action With Confidence

Use the official links below to complete the steps shown in the guide directly on Medicare and Social Security websites.

Medicare Enrollment

🔗 Apply for Social Security Retirement - Official Social Security enrollment portal (Auto-enroll in Medicare Part A and B)

🔗 Enroll in Medicare (Part A & Part B) - Official Medicare enrollment through Social Security

🔗 Withdraw (Un-Enroll) from Medicare Part B - Complete form then make an appointment with Social Security

🔗 Set Up Medicare Easy Pay - Pay Part B premiums if you are not receiving Social Security benefits

Forms Referenced in the Guide

Financial Assistance Programs

🔗 Apply for "Extra Help" (Low-Income Subsidy) - Helps reduce Medicare prescription drug costs

🔗 Apply for a Medicare Savings Program - State-run programs that help pay Medicare premiums and other costs

These links take you directly to official U.S. government websites.

Medicare rules can vary by situation.

If you’d like help confirming the right next step, we’re happy to help.

FAQs

When should I enroll in Medicare if I am turning 65?

Medicare enrollment usually begins during your Initial Enrollment Period. This 7-month window starts three months before your 65th birthday month, includes your birthday month, and continues for three months after.

Enrolling during this time helps you avoid delays and possible penalties.

What is the Medicare Initial Enrollment Period?

The Initial Enrollment Period is a 7-month window when you can first enroll in Medicare Parts A and B.

It begins three months before your 65th birthday month, includes your birthday month, and continues for three months after. Enrolling during this time helps prevent future penalties.

Can I delay Medicare if I am still working at age 65?

In some situations, you may be able to delay Medicare Part B without penalty if you have qualifying coverage through active employment.

Employer size and the type of health plan can affect whether delaying Medicare is allowed.

What happens if I miss my Medicare enrollment deadline?

If you miss your Initial Enrollment Period, you may need to wait for the General Enrollment Period to sign up.

Depending on your situation, you could also face late enrollment penalties that increase your Medicare premiums.

If you’d like a clearer understanding of how Parts A, B, C, and D work together,

you can also review our Medicare 101 guide.

Want a Second Set of Eyes?

If you’d like help confirming the next step based on your situation, we’re happy to help you understand your options.

No pressure. No obligation. Just clarity.

We meet with clients in person throughout the Republic and Springfield area, and offer phone and video consultations for individuals who prefer remote guidance

Maverick Gold

Independent Medicare Advisor

© 2026 Gold Horizon Insurance Solutions. All rights reserved

We are not connected with or endorsed by the United States government or the federal Medicare program. We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

Youtube

Facebook

Instagram

TikTok