Medicare Supplement (Medigap)

Plans Compared

Understanding Your Options Under Original Medicare

Medicare Supplement Insurance, commonly called Medigap, is designed to work alongside Original Medicare (Parts A and B) to reduce out-of-pocket medical costs.

Its purpose is simple:

To help cover certain out-of-pocket costs that Original Medicare does not fully pay.

Medigap policies are offered by private insurance companies but are standardized by the federal government, meaning coverage is the same by plan letter regardless of the carrier.

Each letter represents a different set of benefits.

A Quick Clarification About "Letters"

This is a common source of confusion:

Medicare Parts A, B, C, and D describe how Medicare itself is structured

Medigap Plans (A, B, C, D, F, G, H, etc) are separate policies that help cover costs under Original Medicare

They are completely different systems, even though both use letters.

This page focuses only on Medigap plan letters.

What Medigap Is Designed to Help With

Under Original Medicare, you may still be responsible for:

Deductibles

Coinsurance

Copayments

Extended hospital or skilled nursing costs

Medigap plans help reduce or eliminate many of these expenses, depending on the plan letter you choose.

They do not replace Medicare.

They supplement it.

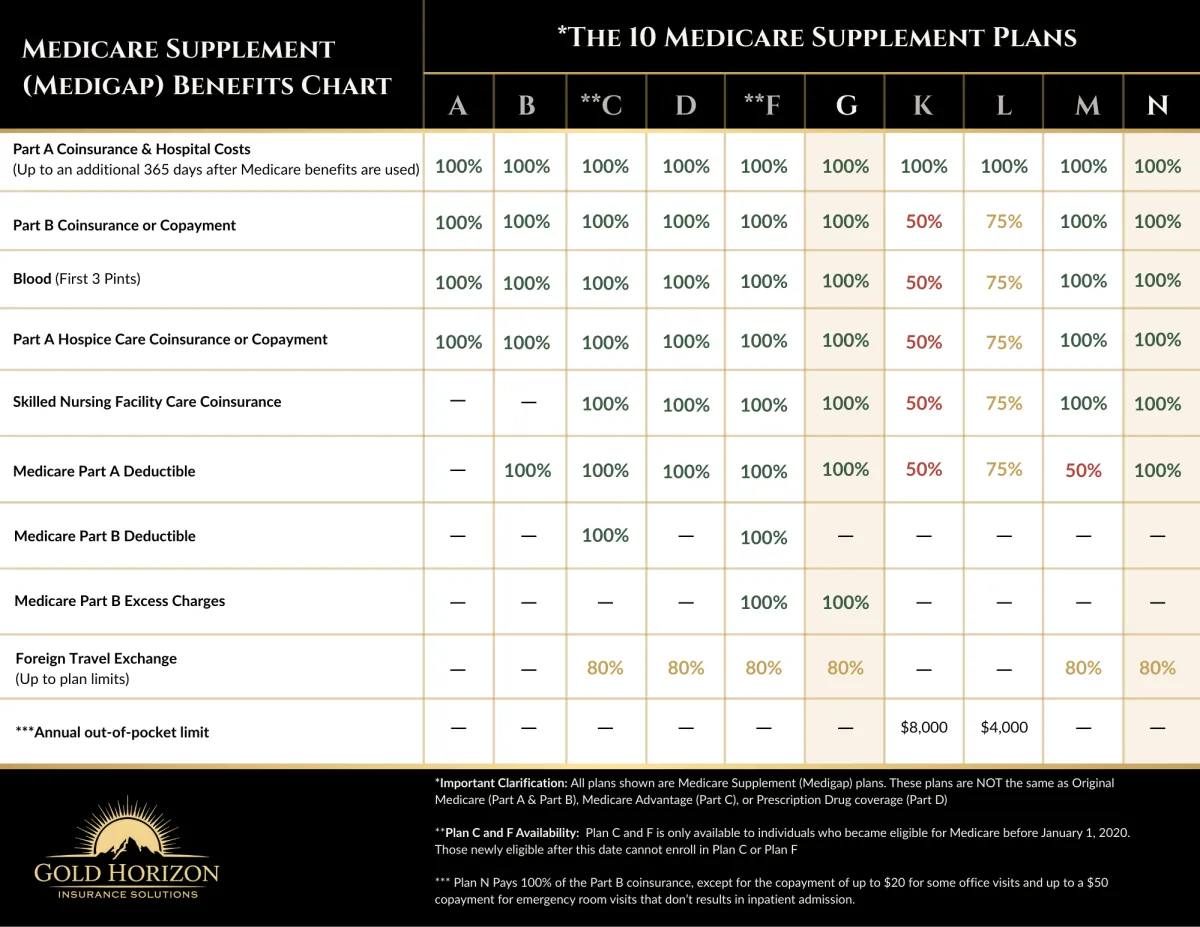

The Medigap Plans at a Glance

Below is a standardized comparison of the Medigap plans currently available.

All insurance companies must follow these benefit rules (the coverage is the same by letter regardless of the carrier.)

Click image below to download 👇

Plans may vary by availability, eligibility date, and location

How to Read This Chart

Each row represents a type of cost under Original Medicare.

Each column represents a Medigap plan letter.

If a box shows 100%, that Medigap plan pays the full amount of that cost after Medicare pays its share.

If a box is blank or marked with a dash, that cost is not covered by that plan.

This chart is meant to show coverage differences, not to suggest one plan is “better” than another.

The Most Commonly Chosen Medigap Plans

While there are multiple plan letters available, most people tend to focus on a few options.

Plan G

• Very comprehensive coverage

• Covers nearly all Medicare-approved out-of-pocket costs

• Does not cover the Part B deductible

Plan G is currently the most popular Medigap plan nationwide because it offers comprehensive coverage with predictable annual costs.

Plan N

• Lower monthly premium than Plan G

• Includes small copays for certain visits

• Does not cover Part B excess charges

Plan N can be a strong option for individuals who prefer lower monthly premiums and are comfortable with occasional copays.

Legacy Plans (C and F)

• Only available to individuals who became eligible for Medicare before January 1, 2020

• Cover the Part B deductible

Availability depends on eligibility date.

Where Gaps Can Still Exist... Even with a Medigap Plan

Medigap plans are designed to help cover medical cost-sharing under Original Medicare, such as deductibles, coinsurance, and copayments.

They work very well for managing medical bills.

What Medigap does not focus on are non-medical or lifestyle-related needs that can arise during illness, hospitalization, or recovery.

These gaps can include:

Dental, vision, and hearing care

Prescription Drugs

Cash support for everyday expenses

Income disruption during a serious illness

Extended hospital stays and daily costs

Help at home during recovery

This isn’t because Medicare or Medigap failed, it’s because they were never designed to handle everything that can happen around a health event.

Some people are comfortable managing these areas on their own.

Others choose to add additional protection, often referred to as Umbrella Coverage, to help soften the financial or logistical impact alongside Medicare and Medigap.

FAQs

What Is the Difference Between Medigap and Medicare Advantage?

Medigap works alongside Original Medicare and helps pay out-of-pocket costs like deductibles and coinsurance. You keep Original Medicare and can typically see any provider that accepts Medicare.

Medicare Advantage replaces Original Medicare and is offered by private insurance companies. These plans usually use provider networks and may include additional benefits like dental or vision.

Can I See Any Doctor With a Medigap Plan?

Yes. Medigap plans allow you to see any doctor or specialist nationwide who accepts Medicare.

Unlike many Medicare Advantage plans, Medigap policies typically do not require provider networks or referrals.

Does Medigap Cover Prescription Drugs?

No. Medigap plans do not include prescription drug coverage.

If you choose Medigap, you usually purchase a separate Medicare Part D plan for prescription medications.

Want Help Making Sense of It All?

If you'd like help understanding:

Which Medigap plans are available to you

How the plans differ in real-world use

Whether additional coverage might make sense

If you're in Missouri, we offer in-person Medigap guidance in the Republic and Springfield area. Phone consultations are also available nationwide.

No pressure. No obligation. Just clarity.

Maverick Gold

Independent Medicare Advisor

© 2026 Gold Horizon Insurance Solutions. All rights reserved

We are not connected with or endorsed by the United States government or the federal Medicare program. We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

Youtube

Facebook

Instagram

TikTok