Medicare Advantage vs Medigap

When people first enroll in Medicare, one of the biggest decisions they face is how to structure their coverage.

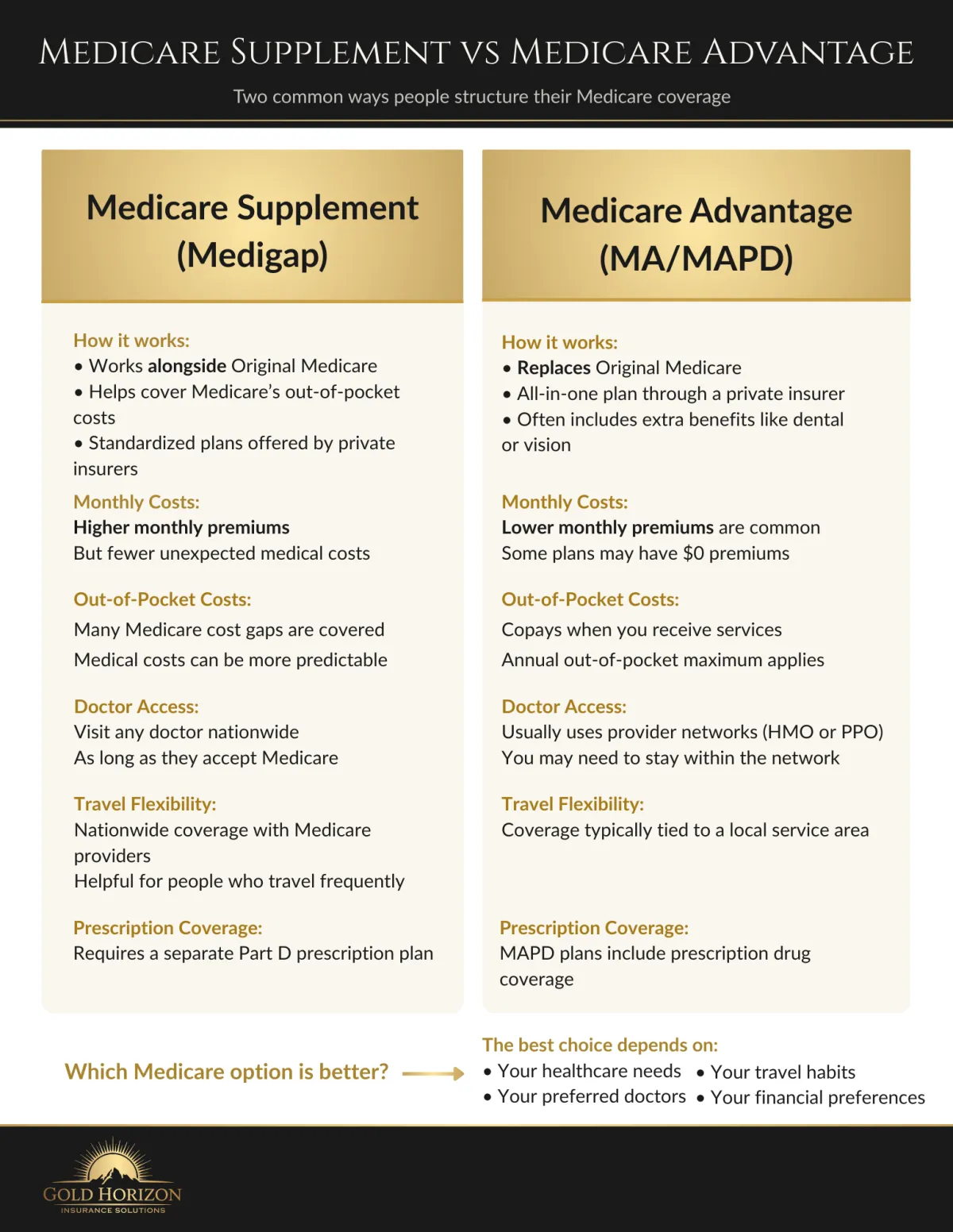

Two of the most common options are Medicare Advantage and Medigap (Medicare Supplement).

Both can help manage healthcare costs, but they work very differently.

Understanding the difference between Medicare Advantage vs Medigap can help you decide which path may better fit your healthcare needs, lifestyle, and financial preferences.

If you're new to Medicare, it may also help to read our guide explaining The ABCDs of Medicare.

Quick Answer:

The biggest difference between Medicare Advantage and Medigap is how you pay for care.

Medicare Advantage plans often have lower monthly premiums but copays when you use services.

Medigap plans usually have higher monthly premiums but fewer out-of-pocket costs when you receive care.

Both options can work well depending on your health needs, travel habits, and financial preferences.

What Medicare Advantage Is

A Medicare Advantage plan (Part C) is offered by private insurance companies approved by Medicare.

These plans replace Original Medicare and combine several types of coverage into one plan.

Most Medicare Advantage plans include:

Hospital coverage (Part A)

Medical coverage (Part B)

Often prescription drug coverage (Part D)

Sometimes dental, vision, or hearing benefits

Medicare Advantage plans usually operate with provider networks, which means you may need to use doctors and hospitals within the network for the lowest costs.

To learn more about how these plans work, visit our page on Medicare Advantage Simplified.

What Medigap Is

Medigap plans are also commonly referred to as Medicare Supplement plans, since they supplement Original Medicare by helping cover certain out-of-pocket costs.

Instead of replacing Medicare, a Medigap policy helps cover the gaps in Medicare, such as:

Deductibles

Copayments

Coinsurance

Medigap plans are standardized, meaning the coverage is the same regardless of which company offers the plan.

One key difference is that Medigap allows you to visit any doctor or hospital nationwide that accepts Medicare, without network restrictions.

For a deeper explanation, visit our Medigap Simplified guide.

Click image below to download 👇

Who Medicare Advantage May Fit Best

Medicare Advantage may be a good fit for people who:

Prefer lower monthly premiums

Are comfortable using provider networks

Want multiple benefits combined into one plan

Like having an annual out-of-pocket limit

Some individuals prefer the simplicity of having their healthcare coverage managed through a single plan.

Who Medigap May Fit Best

Medigap plans may appeal to people who:

Want more predictable healthcare costs

Prefer freedom to choose doctors nationwide

Travel frequently

Want to reduce potential out-of-pocket medical expenses

For many retirees, the flexibility and stability of a supplement plan provides added peace of mind.

How Additional Coverage Can Fit In

Some people also choose to add additional protection alongside their Medicare coverage.

Depending on the plan structure, this may include coverage such as:

Dental insurance

Vision coverage

Hospital indemnity plans

Recovery or short-term care coverage

In some cases, people also review broader protection options like Umbrella Insurance to help protect their assets.

How to Decide Which Path Is Right

There is no single answer to the question "Which Medicare plan is better?"

The right choice depends on several factors, including:

Your current health needs

Your preferred doctors and hospitals

Your travel habits

Your financial comfort with premiums versus out-of-pocket costs

If you are approaching Medicare eligibility, our Turning 65 Medicare Guide can help explain what steps to take first.

It is also important to understand Medicare enrollment periods, since when you enroll can affect your available options.

FAQs

When comparing Medicare Advantage vs Medigap (Medicare Supplement) plans, many people have similar questions. Below are answers to some of the most common questions people ask when deciding which Medicare coverage option may fit their needs.

What is the difference between Medicare Advantage and Medigap?

The biggest difference between Medicare Advantage and Medigap (Medicare Supplement) is how they manage healthcare costs.

Medicare Advantage plans typically have lower monthly premiums but copays when you receive services.

Medigap plans, also called Medicare Supplement plans, usually have higher monthly premiums but help cover many of Medicare’s out-of-pocket costs.

Both options can provide strong coverage, but they work in different ways depending on your healthcare needs and financial preferences.

Which is better: Medicare Advantage or a Medicare Supplement plan?

There is no single Medicare plan that is better for everyone.

Some people prefer Medicare Advantage because the monthly premium is often lower and many benefits are bundled into one plan.

Others prefer Medigap or Medicare Supplement plans because they allow greater flexibility to see doctors nationwide and often reduce out-of-pocket medical costs.

The right option depends on your health needs, travel habits, and financial comfort with monthly premiums versus medical expenses.

Is Medigap the same as a Medicare Supplement plan?

Yes. Medigap and Medicare Supplement plans are the same type of coverage.

The term "Medigap" is commonly used because these plans help cover the gaps in Original Medicare, such as deductibles, coinsurance, and copayments.

Insurance companies and official Medicare materials often use the term Medicare Supplement, but both terms refer to the same type of policy.

Is Medicare Advantage cheaper than Medigap?

Medicare Advantage plans often have lower monthly premiums, and some plans even offer $0 premiums.

However, Medicare Advantage plans typically include copays when healthcare services are used.

Medigap or Medicare Supplement plans usually have higher monthly premiums, but they can reduce or eliminate many out-of-pocket costs when care is needed.

The overall cost depends on how often healthcare services are used and which plan structure fits your situation.

Can I see any doctor with Medigap or Medicare Advantage?

With Medigap or Medicare Supplement plans, you can usually see any doctor or hospital nationwide that accepts Medicare.

Medicare Advantage plans often use provider networks, meaning you may need to see doctors within the plan’s network to receive the lowest costs.

For people who travel frequently or spend time in multiple states, the flexibility of a Medicare Supplement plan can be appealing.

Do Medigap plans include prescription drug coverage?

No. Medigap or Medicare Supplement plans do not include prescription drug coverage.

If you choose a Medicare Supplement plan, you typically enroll in a separate Medicare Part D prescription drug plan.

Many Medicare Advantage plans include prescription drug coverage within the plan itself.

Can I switch from Medicare Advantage to a Medigap or Medicare Supplement plan?

In some cases, people can switch from a Medicare Advantage plan to a Medigap (Medicare Supplement) plan, but approval may depend on timing and health questions.

When you first enroll in Medicare Part B, you receive a six-month Medigap Open Enrollment Period.

During this time, you can enroll in a Medicare Supplement plan without medical underwriting.

After that period, some Medigap plans may require health questions before approval.

Why do some people choose Medigap instead of Medicare Advantage?

Some people choose Medigap or Medicare Supplement plans because they want:

• Predictable healthcare costs

• Freedom to see doctors nationwide

• Flexibility when traveling

Others prefer Medicare Advantage because the monthly premium is often lower and many benefits are bundled into one plan.

Both options can provide reliable Medicare coverage depending on personal needs and preferences.

Need Help Reviewing Your Options?

Choosing between Medicare Advantage and Medigap (Medicare Supplement) plans can feel overwhelming at first.

At Gold Horizon Insurance Solutions, our goal is simply to help you understand your options so you can make a confident decision.

If you would like help reviewing plans available in your area, we are happy to walk through the differences and answer your questions.

Everyone’s situation is different, and the right Medicare plan is the one that fits your healthcare needs and financial preferences.

Maverick Gold

Independent Medicare Advisor

© 2026 Gold Horizon Insurance Solutions. All rights reserved

We are not connected with or endorsed by the United States government or the federal Medicare program. We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

Youtube

Facebook

Instagram

TikTok