Medicare 101

the ABCDs of Medicare Explained Simply

How the ABCDs of Medicare Work (4 Parts)

Medicare is not one single plan.

It is a system made up of four separate parts, each designed to handle a different category of care.

These parts are labeled A, B, C, and D.

The letters describe how Medicare is organized, not how complete your coverage is.

This distinction matters - because many people assume one letter covers more than it actually does.

A Quick Clarification on Medicare Letters

Medicare uses letters.

Medicare Supplement (Medigap) plans also use letters.

They are not the same thing.

Medicare Parts A, B, C, and D describe how Medicare itself is structured

Medigap Plans are optional policies that help cover certain costs Medicare does not fully pay

They serve different purposes and are explained separately to keep things clear.

Why Understanding the 4 Parts Matters

When the letters are misunderstood, people often:

Enroll at the wrong time

Expect coverage that Medicare does not provide

Discover gaps only after a health event occurs

This guide exists to explain what each part does... and what it doesn’t... before decisions are made.

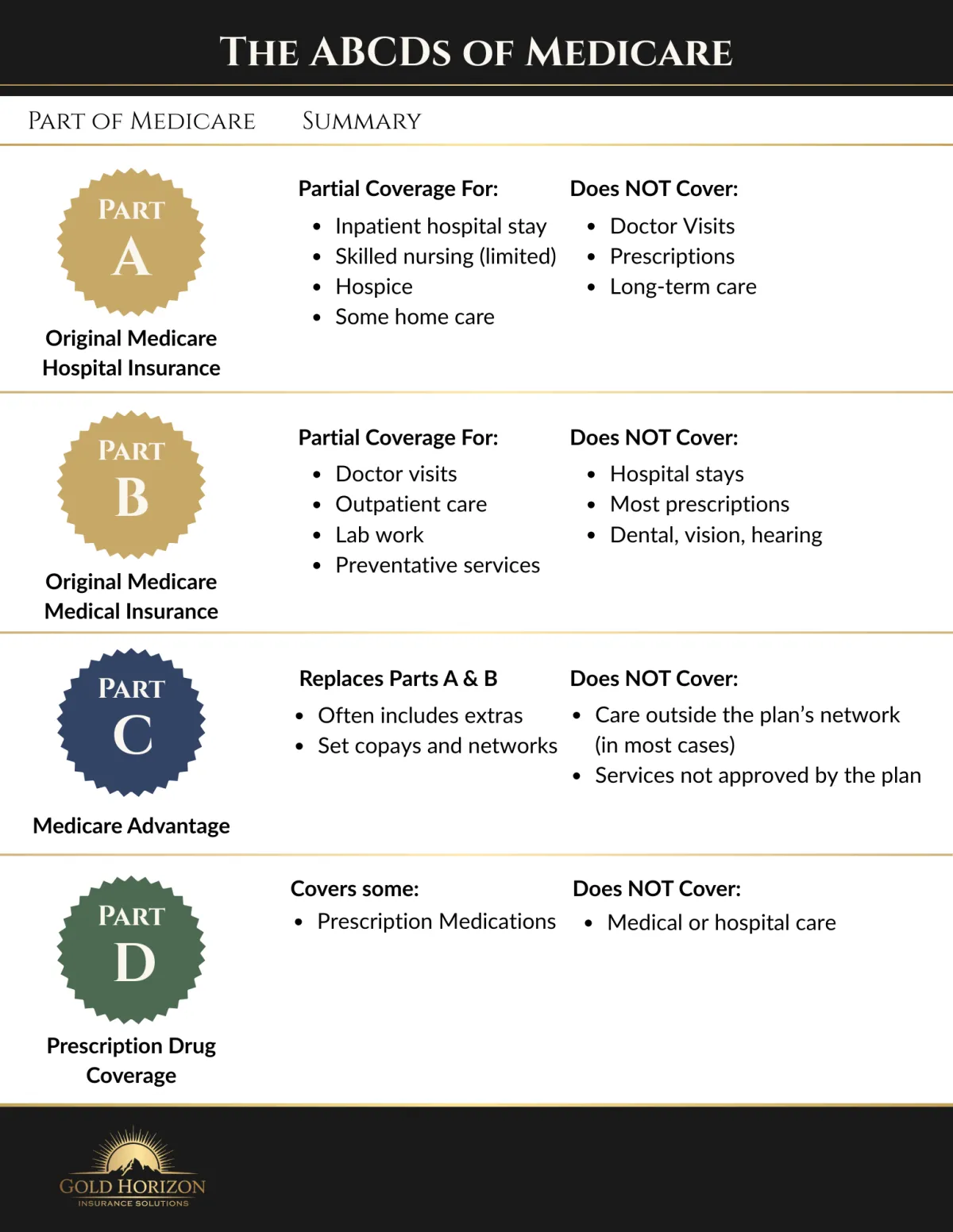

The Four Parts of Medicare at a Glance

The ABCDs of Medicare are the four building blocks of the Medicare system:

Part A - Hospital Coverage

Part B - Medical Services

Part C - Medicare Advantage (an alternative way to receive Parts A and B)

Part D - Prescription drug coverage

Each part works differently.

No single part covers everything.

Click image below to download 👇

This diagram shows how Medicare is divided by function with hospital, medical, prescription drugs, and alternative plan structures.

A Closer Look at Each Medicare Part

Each part of Medicare serves a specific role.

Below, we walk through Parts A, B, C, and D using the same simple framework so you can clearly see what each part covers, and where limitations exist.

Part A - Hospital Insurance

What Part A Covers

• Inpatient hospital stays

• Skilled nursing care (limited duration and conditions)

• Hospice care

• Some home health services

What Part A Does Not Cover

• Doctor visits

• Prescription drugs

• Long-term custodial care

Common Misunderstandings

• “Hospital care is fully covered”

• “Part A handles recovery costs after discharge”

Where Gaps Often Appear

Part A includes deductibles and cost-sharing that are tied to benefit periods, not calendar years. This means costs can reset more than once in a year if hospital stays are separated by time.

While Part A helps cover hospital care, it does not place a cap on out-of-pocket costs for longer or repeated stays. It also does not replace income or help with everyday expenses that often follow a serious illness, heart event, stroke, or extended hospitalization.

Many people who want more predictability around hospital costs explore options that help manage these gaps alongside Original Medicare.

You can learn more in our Medigap Plans Compared guide, or see how some people add Umbrella Coverage to help with costs that Medicare doesn’t address.

Part B - Medical Insurance

What Part B Covers

• Doctor visits

• Outpatient services

• Preventive care

• Lab work

What Part B Does Not Cover

• Hospital stays

• Most prescription drugs

• Dental, vision, and hearing care

Common Misunderstandings

• “Part B is optional with no consequences”

• “Enrollment timing doesn’t matter”

Where Gaps Often Appear

After meeting a deductible, Medicare Part B generally pays 80% of approved medical charges, leaving the remaining portion as the beneficiary’s responsibility.

Original Medicare does not include an annual out-of-pocket maximum. Ongoing care... especially after a serious diagnosis, can involve deductibles, coinsurance, and frequent visits. Medicare helps with medical bills, but it does not provide cash support for everyday expenses during treatment.

To help manage ongoing cost-sharing under Original Medicare, some people choose to add a Medicare Supplement (Medigap) policy. Others also look at additional protection for everyday expenses that Medicare doesn’t cover.

Our Medigap Plans Compared guide and Umbrella Coverage overview explain these options in more detail.

Part C - Medicare Advantage

What Part C Is

• An alternative way to receive Parts A and B

• Offered through private insurance companies approved by Medicare

What Part C Covers

• Hospital and medical services through a private plan

• Often includes additional benefits

What Part C Does Not Cover

• Care outside the plan’s network (in most cases)

• Services not approved by the plan

Common Misunderstandings

• “All Advantage plans work the same”

• “Coverage is guaranteed regardless of provider”

Where Gaps Often Appear

Coverage under Medicare Advantage plans can be affected by provider networks, required approvals, and plan changes from year to year. Extended hospital stays... or recovery at home after discharge... may involve costs or services not fully addressed by the plan.

Medicare Advantage plans manage costs differently than Original Medicare, using networks, approvals, and plan-specific benefits.

To better understand how these plans work in practice, see our Medicare Advantage Guide. Some people also explore Umbrella Coverage to help with recovery-related or out-of-pocket expenses that may fall outside their plan.

Part D - Prescription Drug Coverage

What Part D Covers

• Prescription medications

• Coverage varies by plan

What Part D Does Not Cover

• Medical services

• Hospital care

Common Misunderstandings

• “I don’t need Part D if I take few medications”

• “I can enroll later without penalty”

Where Gaps Often Appear

Prescription coverage focuses on medications, not day-to-day assistance. Medicare focuses on prescription medications, not day-to-day assistance. If managing medications or recovery at home becomes difficult after an illness or hospital stay, in-home support is not covered.

Seeing Gaps as a Whole

Medicare was designed to cover medical care... not every financial or lifestyle impact that can come with illness, hospitalization, or aging.

Depending on how someone receives their Medicare coverage, gaps may appear in areas like:

Income disruption during a serious illness

Extended hospital stays

Recovery and care at home

Dental, vision, and hearing needs

Some people choose to address these gaps through additional protection (often referred to as Umbrella Coverage) designed to support areas Medicare was not intended to cover.

Our Umbrella Coverage page explains these options in more detail and how they are commonly used alongside Medicare.

Want a Second Set of Eyes?

If you’d like help confirming which gaps matter most in your situation, or understanding whether additional protection makes sense, we’re happy to help.

Whether you’re still learning, reviewing options, or ready to enroll, the goal is clarity.

No pressure. No obligation. Just clarity.

Maverick Gold

Independent Medicare Advisor

© 2026 Gold Horizon Insurance Solutions. All rights reserved

We are not connected with or endorsed by the United States government or the federal Medicare program. We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

Youtube

Facebook

Instagram

TikTok