Medicare Advantage:

How Coverage, Networks, & Costs Work

Medicare Advantage plans, also called Medicare Part C plans, can look simple at first glance.

Low premiums. Extra benefits. An annual out-of-pocket limit.

But how these plans actually work day-to-day matters just as much as what shows up on a brochure.

This page explains, in plain language:

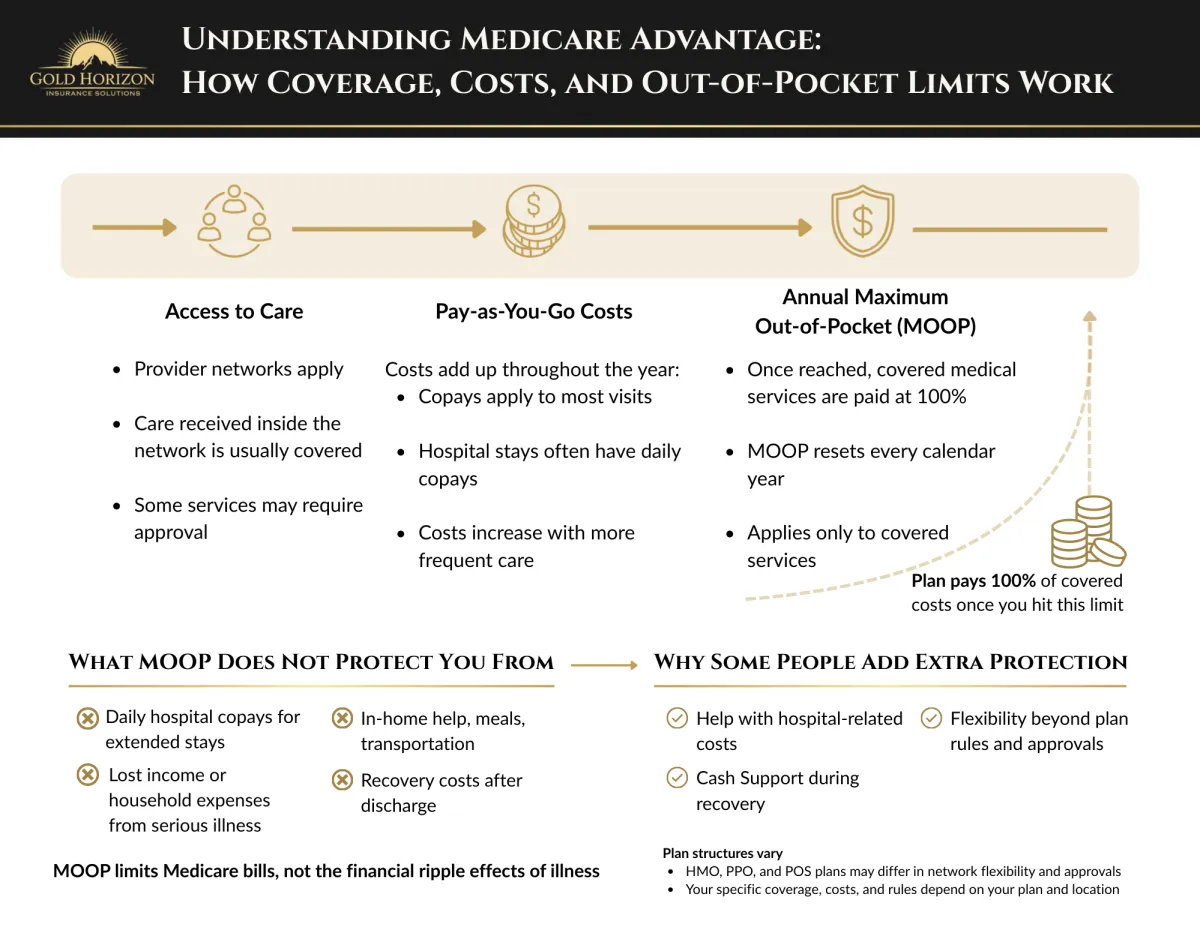

How access to care works

How costs add up when care is used

What the out-of-pocket maximum does (and does not) protect you from

No plan recommendations here, just clarity

What Medicare Advantage is

Medicare Advantage (also called Part C) is an alternative way to receive your Medicare benefits.

Medicare Advantage plans are offered by private insurance companies approved by Medicare and are available in most counties nationwide. Instead of Original Medicare paying first, your care is managed through a private insurance plan approved by Medicare.

These plans combine:

Hospital coverage (Part A)

Medical coverage (Part B)

Often prescription drug coverage (Part D)

All in one plan.

Medicare still oversees the rules, but the plan controls how care is accessed and how costs are applied.

How Medicare Advantage Works in Real Life

Medicare Advantage plans don’t work like traditional insurance where you pay a premium and most costs disappear.

Instead, they are designed around managed access and pay-as-you-go care.

That means:

How you access care matters

Costs are spread out over time

Protection comes from an annual limit, not predictable bills

Most Medicare Advantage plans follow the same three-part structure, even though the details vary by plan and location.

Understanding these three parts will help you understand where costs come from and why some people feel surprised later.

Click image below to download 👇

Plans may vary by availability, eligibility date, and location

Access to Care

(Networks & Approvals)

Medicare Advantage plans use provider networks.

This means:

Care received inside the network is typically covered

Care received outside the network may cost more or not be covered at all

Some services may require approval before care is provided

Depending on the plan type (HMO, PPO, or POS), you may:

Need to choose a primary doctor

Need referrals for specialists

Have limited or partial out-of-network access

Access rules don’t usually affect care during routine years, they matter most when care becomes frequent or complex.

Pay-As-You-Go Costs

(Copays & Coinsurance)

Medicare Advantage plans typically have lower monthly premiums, but costs show up when care is used.

Instead of large upfront costs, you may see:

Copays for doctor visits

Daily copays for hospital stays

Separate copays for specialists, urgent care, or emergency services

These costs:

Apply each time care is used

Add up throughout the year

Increase during high-use or extended health events

In low-use years, expenses may stay minimal.

In high-use years, costs can accumulate quickly.

Annual Maximum Out-of-Pocket

(MOOP)

Medicare Advantage plans include an annual maximum out-of-pocket limit, often called the MOOP. The Medicare Advantage out-of-pocket maximum applies only to covered medical services and does not include prescription drug costs under Part D.

This limit:

Caps how much you’ll pay for covered medical services in a calendar year

Applies only to in-network, covered care

Resets every January 1

Once you reach this limit:

The plan pays 100% of covered medical costs for the rest of the year.

The MOOP provides important protection, but it does not eliminate all financial exposure.

What the MOOP Does Not protect you from

The Maximum Out-of-Pocket limit is an important safeguard, but it only applies to covered medical services.

It does not protect against many common financial stress points that often follow a serious health event, including:

Daily hospital copays during extended stays

Recovery costs after discharge

In-home help, meals, or transportation

Lost income or household expenses during illness

In practice this means:

The MOOP limits Medicare bills not the full financial impact of a medical event.

Our Guidance on Medicare Advantage Coverage

Because of these gaps, we generally do not recommend enrolling in a Medicare Advantage plan without some form of umbrella coverage in place.

This isn’t because Medicare Advantage plans are “bad.”

It’s because:

Costs are unpredictable in high-use years

Recovery expenses are rarely planned for

Financial strain often comes from outside the medical bill itself

Umbrella coverage helps address the areas Medicare Advantage was never designed to cover.

Why Many People Choose Umbrella Coverage with Medicare Advantage

People add umbrella coverage for different reasons.

Some of the most common include:

1. Limited Savings for a Sudden Health Event

Not everyone wants to self-insure thousands of dollars in unexpected costs.

Umbrella coverage can reduce the need to tap savings during an already stressful time.

2. Protection Against Recovery & Daily Living Expenses

Cash benefits can help with:

Hospital-related costs

Recovery at home

Transportation, meals, or short-term assistance

3. A “DIY Medigap” Approach with More Control

Some people want:

Predictable monthly expenses

Flexibility in how benefits are used

Fewer underwriting hurdles than traditional Medigap

In many cases, umbrella coverage can replicate a large portion of what Medigap does, while allowing the individual to control:

Monthly cost

Benefit focus

Level of protection

It’s not the same as Medigap, but for the right person, it can be a practical, flexible alternative.

Learn More About Your Options

If you’d like to explore these options further, you may find these resources helpful:

Umbrella Coverage Overview

How hospital indemnity, recovery, and cash-based benefits can help soften the financial impact alongside Medicare Advantage.The ABCDs of Medicare

A clear breakdown of how Parts A, B, C, and D work together (and where gaps can exist).Turning 65: Your Medicare Decision Guide

A step-by-step overview of the choices most people face when first enrolling in Medicare.

FAQs

Is Medicare Advantage the Same as Original Medicare?

No. Medicare Advantage plans replace Original Medicare (Parts A and B) and are offered by private insurance companies approved by Medicare.

These plans must cover everything Original Medicare covers, but they may include additional benefits such as dental, vision, or hearing coverage.

Do Medicare Advantage plans use provider networks?

Yes. Most Medicare Advantage plans use provider networks such as HMOs or PPOs.

This means you may need to use doctors and hospitals within the plan’s network to receive the lowest costs for care.

What is the maximum out-of-pocket cost for Medicare Advantage plans?

Medicare Advantage plans include an annual maximum out-of-pocket limit for covered medical services.

Once you reach that limit during the year, the plan pays 100 percent of covered costs for the rest of the year.

Want Help Making Sense of It All?

If you'd like help understanding:

Whether Medicare Advantage fits your situation

What gaps may exist in your current setup

Whether umbrella coverage or Medigap makes more sense for you

If you're in Missouri, we offer in-person guidance in the Republic and Springfield area. We also provide phone consultations for individuals nationwide.

No pressure. No obligation. Just clarity.

Maverick Gold

Independent Medicare Advisor

© 2026 Gold Horizon Insurance Solutions. All rights reserved

We are not connected with or endorsed by the United States government or the federal Medicare program. We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

Youtube

Facebook

Instagram

TikTok